The market has been hit over the past week due to the U.S. and Iran conflict. The question is if...

At Virtus Wealth Management, your Southlake independent financial advisors, we help our clients prepare for a financially-secure future by developing long-term strategies that focus on the “big picture” versus short-term gain, thereby managing risk.

Today’s economic conditions and uncertain financial markets require the savvy investor to go beyond traditional boundaries.

Our mission is to provide innovative, sophisticated and highly customized wealth management solutions and financial advice that address all facets of your finances.

We tailor everything to each of our clients’ specific needs so that each client can pursue his or her different goals.

Virtus Wealth Management is the product of a 2016 merger between two well-established Texas wealth management firms.

Wealth management is more than just investment advice – it includes all aspects of a client’s financial life.

The market has been hit over the past week due to the U.S. and Iran conflict. The question is if...

In my last article, I discussed the importance of proper titles in regards to qualified accounts,...

Wealth management is more than just investment advice – it includes all aspects of a client’s financial life.

At Virtus Wealth Management, we believe we can help you no matter what age you are, what life stage you are in, or how much money you are working with. We want you to feel educated, empowered, and involved in the planning of your financial future.

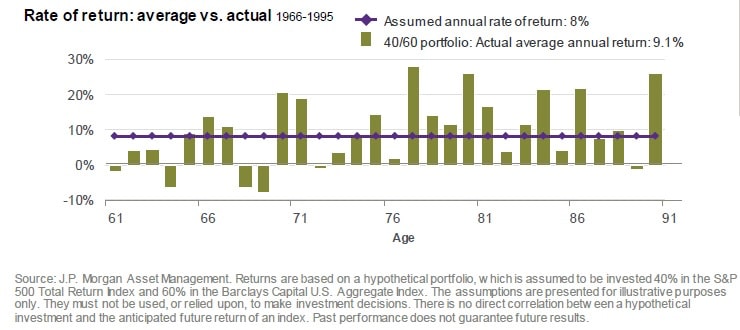

Relying on averages can be dangerous. Brian’s dad had a saying, “You can drown in a river that averages 3 feet deep.” Using averages can be risky, and applies to retirement planning too.

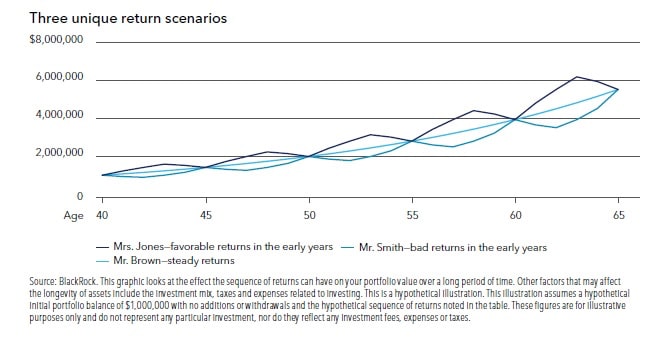

During the accumulation phase of retirement planning, the impact of sequence of returns can be minimal (See Charts Below).

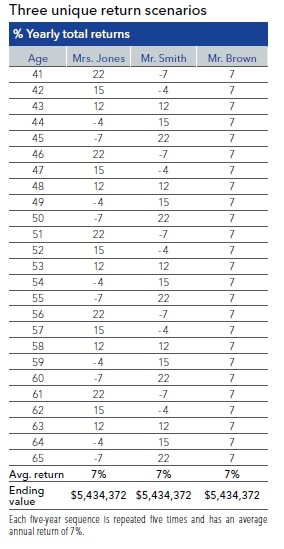

Three investors made the same initial hypothetical investment of $1,000,000 at age 40 with no additions or withdrawals.

All had an average annual return of 7% over 25 years. However, each experienced a different sequence of returns.

At age 65, all had the same portfolio value, although they had experienced different valuations along the way.

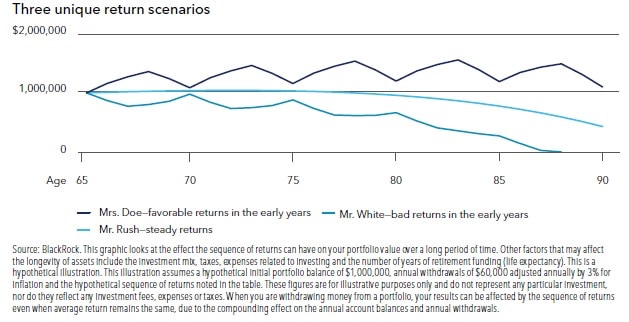

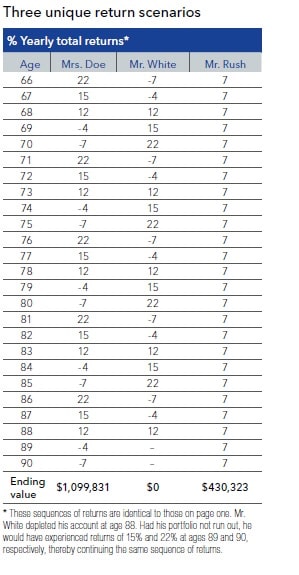

During the withdrawal phase, it’s a different story. The sequence of returns can have a critical impact on portfolio value due to the compounding effect on the annual account balances and annual withdrawals (See Charts Below).

Withdrawing assets in down markets early in retirement can ravage a portfolio. How do you counter your Sequence of Return risk? Here at Virtus Wealth Management we use several techniques including considering a dynamic approach to spending and strategies that incorporate downside risk management. There is one thing for certain … the market does not work in averages (see final chart below); we help our clients proactively prepare accordingly.

No strategy assures success or protects against loss. Investing involves risk including loss of principal.

Some of this material was prepared by Blackrock.